How to Make Estimated Tax Payments

Understanding the nuances of quarterly estimated tax payments is crucial for individuals and businesses alike. This guide walks you through who needs to pay, how to make your federal and California payments online step by step, when payments are due, and what happens if you miss them. Our goal is to make the process simple, even if this is your first time paying online.

Who Needs to Make Quarterly Tax Payments?

Estimated tax payments are mainly for taxpayers whose income is not subject to withholding. This includes self-employed individuals, investors, landlords, and people with significant income from dividends, interest, alimony, or capital gains. S corporation shareholders may also owe estimated taxes.

If you expect to owe $1,000 or more in income tax when you file your individual return, the IRS generally requires you to make estimated tax payments. Corporations generally must pay if they expect to owe $500 or more.

If you did not owe income tax in the prior year, you generally are not required to make estimated payments. Keep in mind that the IRS does not send a reminder telling you to start paying. It is up to each taxpayer to determine whether payments are required and to make them on time.

Before You Start: What to Have Ready

Gathering a few items first makes the online process much smoother:

- Your Social Security number or ITIN. If you file jointly, have both spouses’ numbers.

- Your bank routing and account numbers. These are at the bottom of a check or in your online banking app. Know whether the account is checking or savings.

- A prior-year tax return. The IRS confirms your identity using information from a past return (more on this below), so keep one within reach.

- Your payment amount. If we prepared your return, the amount for each quarter is listed in the cover letter included with your tax materials.

- The tax year and quarter you are paying. For payments made during 2026, you are generally paying toward the 2026 tax year.

How to Make Federal Quarterly Estimated Tax Payments Online

Watch the video below to make your federal tax payments. Written instructions found below.

- Go to https://www.irs.gov/payments

- You can select:

- Pay Now with DirectPay: Pay without creating an account with the IRS via your bank account.

- Pay by Debit Card, Credit Card, or Digital Wallet: Pay without creating an account with the IRS via a card.

- Sign in to Pay: Create or use your ID.me account. At Evolution Tax & Legal, we recommend you create an Id.me account with the IRS to submit your payments. With an account, you can view your payment history, schedule future payments, and view the amount you owe among other benefits.

- Follow the steps for your previous selection. Make sure you select “Estimated Tax” for the “Payment Selection” dropdown.

We generally recommend the Online Account for clients who want everything in one place. If that feels like too many steps, Option 1 (Direct Pay) gets the same payment made without an account.

How to Make Your California Payment Online (FTB Web Pay)

If you owe California estimated taxes, the Franchise Tax Board’s Web Pay service lets you pay directly from your bank account for free.

- Go to ftb.ca.gov/pay and choose Bank account (Web Pay).

- Select “Estimated Tax Payment (Form 540-ES)” as the payment type and the 2026 tax year.

- Verify your identity with information from a recent California return, enter your bank details and payment amount, then review and submit. You can use Web Pay without a MyFTB account, though a MyFTB login lets you track history.

Paying in Another State

If you file in a state other than California, most states have their own free online payment portal. You can find your state’s tax agency and payment site through the IRS state government websites directory.

When are Estimated Quarterly Taxes Due for 2026 Tax Year?

For the 2026 tax year, the quarterly estimated tax due dates are:

- April 15, 2026

- June 15, 2026

- September 15, 2026

- January 15, 2027 (final payment for the 2026 tax year)

All four dates fall on a regular business day this year, so none are pushed back. If a due date ever lands on a weekend or legal holiday, it shifts to the next business day. California uses these same dates.

Can I Pay Estimated Taxes Annually Instead of Quarterly?

Yes. You can pay your full estimated tax at once rather than in four installments. If you choose to do this, submit the full amount by the first quarterly deadline so you do not accrue interest for missing the earlier installments.

What Happens if I Fail to Make My Estimated Payments?

Not making your estimated quarterly tax payments can lead to several consequences, both at the federal and state levels, though the specifics can vary depending on the jurisdiction and the rules of the tax authority. Here’s what generally happens if you don’t pay your estimated quarterly taxes due:

Federal Taxes:

- Underpayment Penalty: The IRS can impose an underpayment penalty if you don’t pay enough tax through withholding or estimated tax payments, or if you don’t pay on time. The penalty is essentially an interest charge on the amount you underpaid, calculated for the period you underpaid.

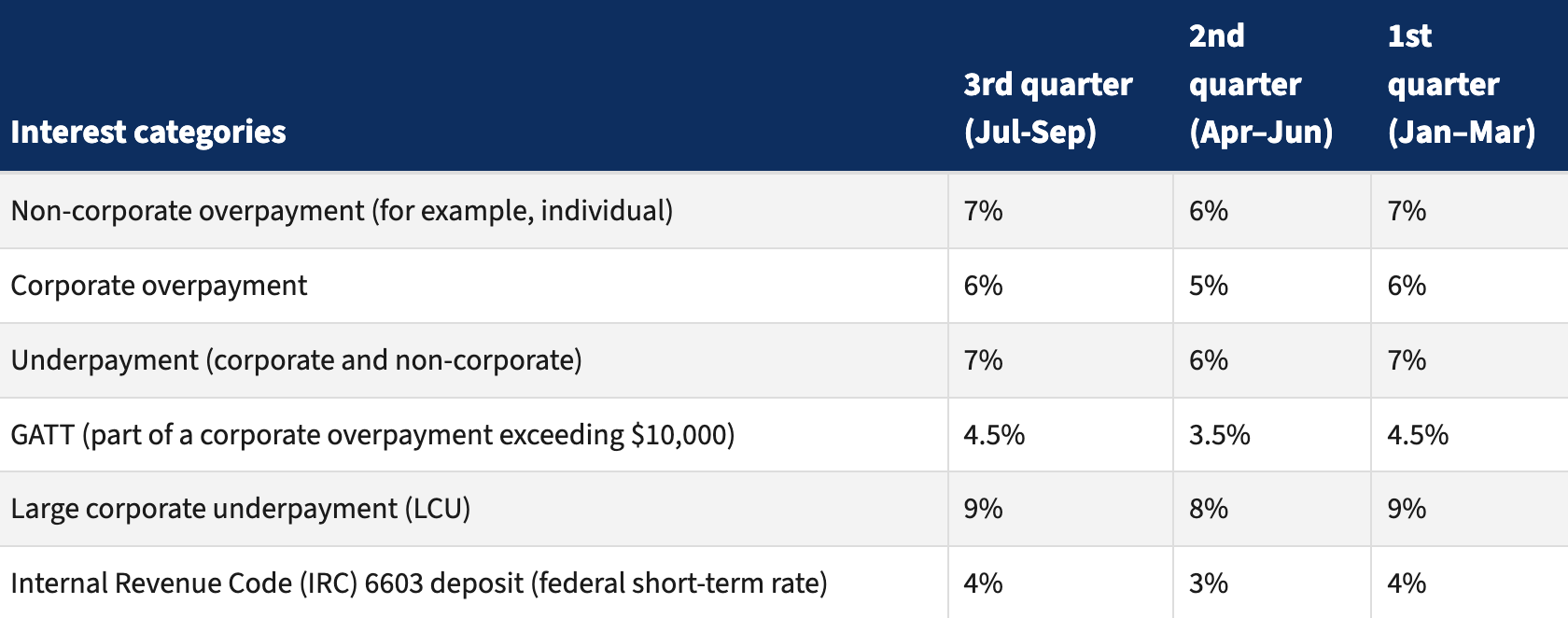

- Interest Charges: Beyond penalties, interest accrues on any unpaid tax from the due date of the return until the date of payment in full. The interest rate is determined quarterly and is the federal short-term rate plus 3%.

- Large Tax Bill: If you don’t make estimated payments or withhold enough tax, you might face a surprisingly large tax bill when you file your annual return, potentially leading to financial strain.

- Tax Liens or Levies: In severe cases, if significant taxes are owed and not paid, the IRS might enforce collection through tax liens against your property or levies on your bank accounts or wages.

What are the current Federal Interest Rates?

You can check the current figure on the IRS quarterly interest rates page.

State Taxes:

- Penalties and interest. Most states impose their own penalties and interest for underpayment or late payment.

- Different rules and rates. Each state sets its own thresholds, rates, and methods, so the details vary.

- Collection actions. States can also pursue liens, levies, and wage garnishment for unpaid amounts.

Safe Harbor

Both the federal and many state systems offer safe harbor rules. You generally avoid an underpayment penalty if you pay a set percentage of what you owe (commonly 90% to 110%, depending on your situation) or an amount based on your prior-year tax. If we prepared your return, we provide your estimated payment amounts based on your prior-year filing. If your income changes during the year, you may need to adjust your payments.

How to Calculate My Quarterly Payment?

Use IRS Form 1040-ES to calculate quarterly tax payment using your estimated taxes. This form includes a worksheet that helps you estimate your income, deductions, and credits for the year. Based on this estimate, you’ll determine the amount of tax you expect to owe and then divide this amount by four to find your quarterly payment amount.

Better yet, if you worked with a CPA or tax attorney for your previous year’s tax filing, they should provide you this information. At Evolution Tax & Legal, you will find the amounts on your cover letter.

How a Tax Professional Can Help with Quarterly Payments

At Evolution Tax & Legal, we are uniquely positioned to help individuals and businesses successfully navigate tax law, ensuring you stay compliant while optimizing your financial strategy. We help by:

Accurate Calculation of Estimated Taxes

- Income Estimation: Our team accurately estimates your income for the year, which is crucial for determining your estimated tax payments.

- Tax Liability Analysis: We calculate your total tax liability, taking into account all potential deductions, credits, and exclusions you’re eligible for, ensuring that your estimated payments are as accurate as possible.

Avoiding Penalties and Interest

- Safe Harbor Guidelines: We help you apply safe harbor rules, ensuring you pay enough tax throughout the year to avoid underpayment penalties.

- Adjusting Payments: We assist in adjusting your estimated tax payments throughout the year in response to changes in income, deductions, or tax law, helping you avoid overpayment or underpayment.

Tax Planning and Strategy

- Future Tax Planning: Our tax experts provide strategies for tax efficiency, advising on ways to defer income, accelerate deductions, or take advantage of tax credits and deductions.

- Year-Round Consultation: We offer ongoing advice and update you on tax law changes that might affect your estimated tax payments or overall tax strategy.

Representation and Dispute Resolution

- IRS Representation: If there are any discrepancies or disputes with the IRS regarding your estimated payments, our tax attorneys can represent you, helping to resolve issues efficiently and effectively.

- Audit Support: In the case of an audit, having our team of tax professionals who are familiar with your financial situation and tax payments can be invaluable.

FAQs

What is the qualified business income deduction and how does it affect quarterly tax payments?

The Qualified Business Income (QBI) deduction, also known as the Section 199A deduction, can impact your estimated tax payments, but it doesn’t directly relate to the requirement to make these payments. Rather, it affects the amount of income that is subject to tax, which in turn influences how much you should pay in estimated taxes. In short, the QBI deduction may lower your tax liability.

The QBI deduction allows eligible self-employed individuals, sole proprietors, and pass-through business owners (such as partnerships, S corporations, and some trusts and estates) to deduct up to 20% of their qualified business income, plus 20% of qualified real estate investment trust (REIT) dividends and qualified publicly traded partnership (PTP) income. This deduction effectively reduces your taxable income, thereby potentially lowering your tax liability.

Given the complexities surrounding the QBI deduction and its impact on your overall tax situation, consulting with a tax professional is advisable.

What is the 110% rule for estimated tax payments?

The 110% rule for estimated tax payments is a guideline set by the IRS that applies to individuals who are calculating their estimated taxes, particularly those with higher incomes. This rule is part of the safe harbor provisions designed to help taxpayers avoid underpayment penalties. Taxpayers can pay estimated taxes equal to 100% of the tax shown on their current year’s return or 110% of the tax shown on their prior year’s return, whichever is smaller.

This article is for informational purposes only and does not constitute legal or tax advice. Tax laws and regulations change frequently and may affect the accuracy of this information. Consult a qualified tax attorney or CPA before making any decisions based on the content of this article. Schedule a consultation.

June 10, 2026

Posted on

ready to get started?

schedule your free consultation today!

Expect to hear from our team in less than 24 hours.

schedule your free consultation today!